BI Intelligence

BI IntelligenceSee Also

This story was delivered to BI Intelligence “Payments Briefing” subscribers. To learn more and subscribe, please click here.

Same-day ACH, the US faster payments initiative to speed up settlement times for a specific class of bank-based transactions, is off to a strong start following initial implementation in late September, according to new data from NACHA, the electronic payments association.

In October, same-day ACH was responsible for 3.8 million transactions worth just under $5 billion.

Those figures mark “strong use,” and are consistent with NACHA expectations, but point to demand in the market that the system can fulfill. And it’s likely that pickup will remain moving at a fast pace, particularly since NACHA found that 95% of top ACH-originating institutions plan to implement the initiative by the end of this year.

Though the initiative saw strong uptake across categories, same-day ACH for business-to-business (B2B) payments is worth paying particular attention to.

- B2B was the second most-popular use case for ACH in October. B2B payments were responsible for 36% of same-day ACH volume in October. For context, that’s 1.4 million transactions worth $2.8 billion — closely behind the figures that direct deposit, the most popular function, posted.

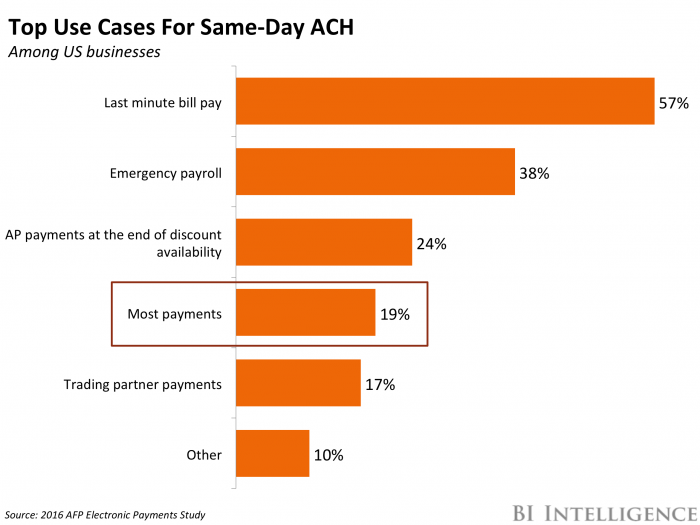

- There’s likely a long runway for growth in the B2B space. Right now, a large portion of businesses still conduct most of their payments via check. That’s due to a variety of factors, but it’s plausible that the ACH settlement lag contributes to it. Around the time of the launch of the first phase of same-day ACH, 19% of businesses planned to use it for “most of their payments” and 62% believed the initiative will have a somewhat or extremely positive impact. Strong pickup in the first month re-emphasizes the need for faster payments in this segment in particular, and indicates that it could lead to major increases in the percentage of B2B payments conducted electronically moving forward.

In the US, when customers make payments via banks, they’re completed in two ways: via wire transfer, or through the Automated Clearing House (ACH). ACH transactions, which are less expensive for customers and which accounted for 18% of total noncash US payments volume in 2012, can take up to five days to settle because of the way that they are processed.

That’s problematic, because it interferes with consumer demand for convenience and could slow the supply chain or make it more challenging for banks and businesses to get paid in the way they need to conduct operations. As a result, the US Fed looked into the ACH system in 2013, and found that there was no “ubiquitous, convenient, and cost-effective way for US consumers and businesses to make fast payments between banks.

In response, the Fed, NACHA, and private institutions have begun to find ways, together and separately, to modernize the US payments system in order to increase convenience and catch up to many of the country’s trade partners. The Fed has formed a task force, which will resolve potential solutions, while NACHA and private institutions are pushing banks to hit a set of three same-day settlement deadlines through late 2016 and into 2017. Such a system will particularly benefit high-growth spaces in the electronic payments ecosystem, like P2P and B2B payments, which could magnify its impact over time.

Though it’s likely the system could grow ACH volume by making it a more appealing option in these high-growth areas, it could become a hindrance to banks. That’s because the implementation is costly and time-consuming — the Fed find that the business impact is net-neutral to negative for these firms. Instead, the parties that reap these benefits are providers of services in these high growth areas, like mobile bill pay firms or P2P vendors, which means that banks are actually aiding their competitors. That means that Faster Payments could ultimately enhance the impact of digital disruption in the payments ecosystem, rather than mitigate it.

Jaime Toplin, research associate for BI Intelligence, Business Insider’s premium research service, has compiled a detailed report on faster payments that looks at why the US needs a Faster Payments system, explains how the country plans to implement it, evaluates the different areas that are most likely to be impacted by Faster Payments, and determines which parties benefit from such a system and which are hindered by it.

Here are some key takeaways from the report:

- Sluggish settlement of payments in the US is pushing NACHA, the national electronic payments trade group, and the Federal Reserve to reform the system. US payments made via ACH can take three to five days to settle.The Fed’s Faster Payments Task Force and NACHA are looking to implement a same-day settlement program in the US by 2017 in order to increase consumer convenience.

- The number of transactions affected by faster payments will increase over time.Four key areas — P2P, B2B, C2B, and B2C payments — will gain the most from such a system. And these areas, which comprised 12% of US payments volume in 2014, will grow rapidly over time, therefore magnifying the impact of such a system.

- Faster payments implementation will be a mixed bag for banks, because of additional costs associated with the burden of implementation. And the platform is likely to actually boost third-party providers, like P2P app vendors or mobile bill pay firms, by giving them an easy way to increase efficiency, engagement, and volume, without a substantial rise in transaction costs.

In full, the report:

- Explains how the US payments system works and why it needs to be modernized

- Defines Faster Payments and lays out how the country plans to implement such a system

- Explores different high-growth areas in the payments ecosystem and the impact Faster Payments could have on them

- Evaluates whether or not such a system will be useful for banks and financial institutions

- Determines the beneficiaries of Faster Payments and the impact it may have

Interested in getting the full report? Here are two ways to access it:

- Subscribe to an All-Access pass to BI Intelligence and gain immediate access to this report and over 100 other expertly researched reports. As an added bonus, you’ll also gain access to all future reports and daily newsletters to ensure you stay ahead of the curve and benefit personally and professionally. >>START A MEMBERSHIP

- Purchase & download the full report from our research store. >> BUY THE REPORT

EXCLUSIVE FREE REPORT:

EXCLUSIVE FREE REPORT:5 Top Fintech Predictions by the BI Intelligence Research Team. Get the Report Now »